Plus Two Economics-Chapter 9

Chapter 9:-

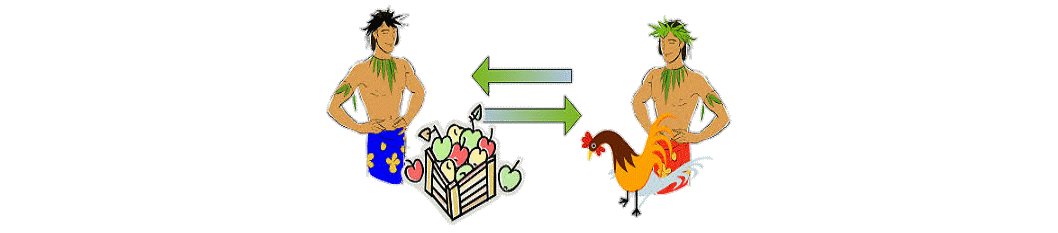

Introduction Invention of money is regarded as one of the greatest inventions of man. Modern economy is called money economy. It is difficult to think of life without money. But, it is important to note that there was a time when money did not exist. In the olden days, economic life was very simple. Human wants were very limited. The family and society were self sufficient. Therefore, there was no need for exchange. With the Passage of time, human wants multiplied. It became impossible to Produce everything that one needed. This led to specialisation. As a result, exchange emerged. Man started exchanging commodities for commodities. This system of exchange is known as the barter system.

Barter System The system in which one commodity is exchanged for another is called barter system. For example, people bought a cow in exchange for a sack of paddy, or exchange paddy for vegetables and food grains. This system of economy wherein goods were exchanged for other goods is known as C – C Economy, i.e., commodities are exchanged ‘for commodities.

Difficulties of Barter System

1. Absence of double coincidence of wants

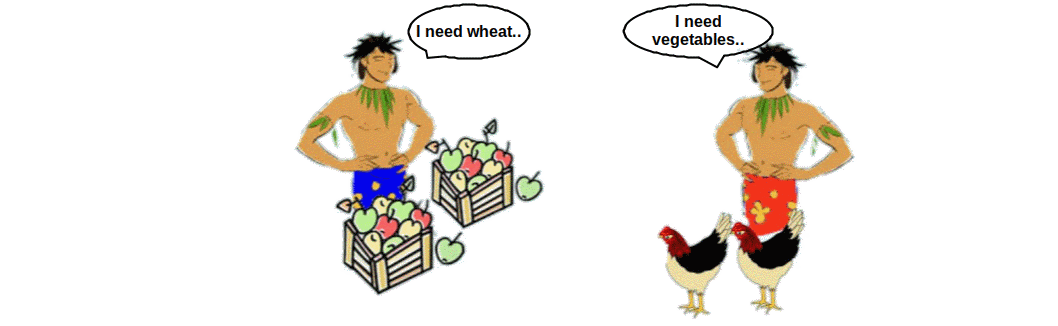

Barter system works smoothly only if the wants of the buyer and the seller coincide. For example, if a person wants to sell cloth to buy rice, he has to find a person who-wants to sell rice and buy

cloth. But if one wants to sell rice and buy vegetables, the transaction will not take place. This difficulty of double coincidence: of wants is a major drawback of the barter system.

Barter system works smoothly only if the wants of the buyer and the seller coincide. For example, if a person wants to sell cloth to buy rice, he has to find a person who-wants to sell rice and buy

cloth. But if one wants to sell rice and buy vegetables, the transaction will not take place. This difficulty of double coincidence: of wants is a major drawback of the barter system.

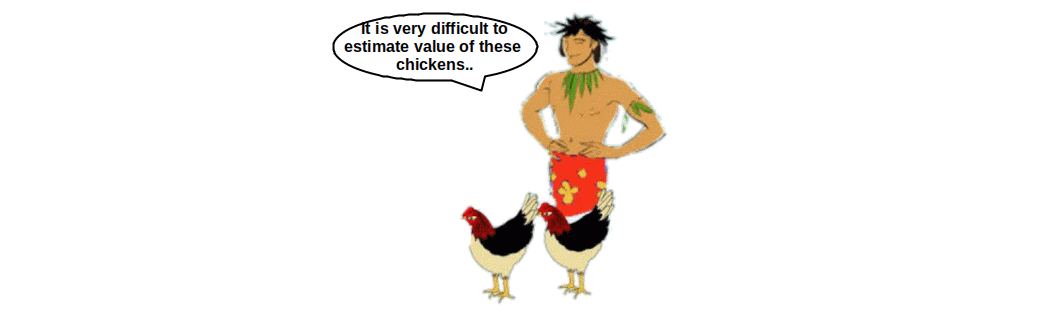

2. Absence of common measure of value

Under the barter system there is no common measure of value. Different goods are exchanged on different measures of value.

Under the barter system there is no common measure of value. Different goods are exchanged on different measures of value.

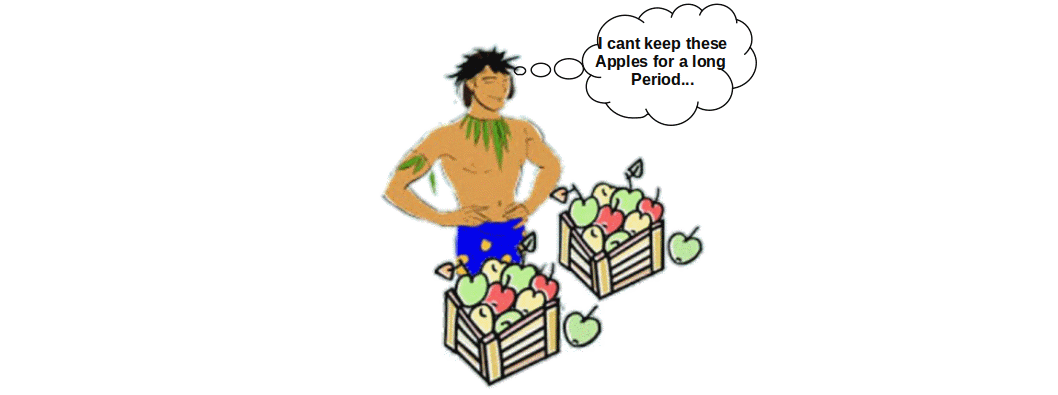

3. Lack of store of value

Under the ‘barter. System,’ a Person’s wealth is stored only in the form of commodities. Most of the commodities are not durable. So they cannot be stored for a long time. Moreover, they require a lot of storing space. This is another drawback of barter system.

Under the ‘barter. System,’ a Person’s wealth is stored only in the form of commodities. Most of the commodities are not durable. So they cannot be stored for a long time. Moreover, they require a lot of storing space. This is another drawback of barter system.

4. Lack of standard of deferred payments

This means there is no standard basis for borrowing and lending. For example, if a cow is borrowed, its value changes at the time it is returned to the lender. The value may be increased or decreased.

This means there is no standard basis for borrowing and lending. For example, if a cow is borrowed, its value changes at the time it is returned to the lender. The value may be increased or decreased.

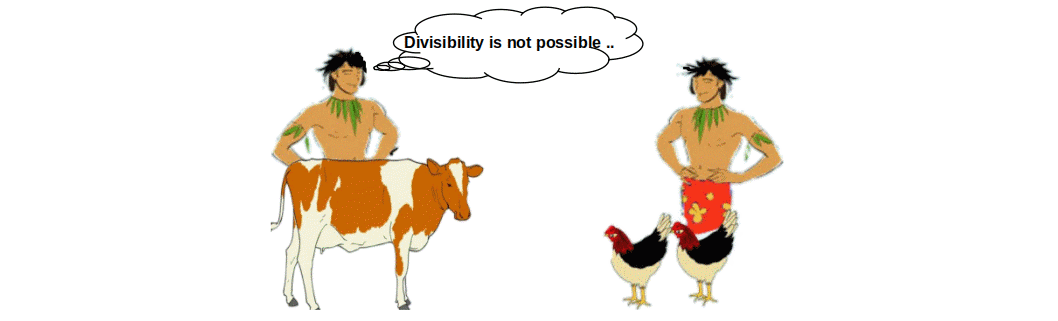

5. Problems of indivisibility

Some goods cannot be divided. For example, if the exchange for a cow with a bag of paddy, and if only half a bag of paddy is needed, the cow cannot be divided. To solve such a problem of the

barter system man was on search for a new way. This led to the emergence of money.

Some goods cannot be divided. For example, if the exchange for a cow with a bag of paddy, and if only half a bag of paddy is needed, the cow cannot be divided. To solve such a problem of the

barter system man was on search for a new way. This led to the emergence of money.

What is Money? Economists have given different definitions for money. According to the legal definition, money is any thing generally accepted. Walker defines money as “Money is what money does”. Therefore, money is defined as anything which is generally accepted as a medium of exchange, measure of unit of account, store of value and a standard for deferred payments.

Functions of Money Money performs many useful functions. These functions can be broadly classified into three. They are:

I. Primary Functions 1. A medium of exchange

2. A measure of valueII. Secondary Functions 3. A store of value

4. A standard of deferred payments 5. A transfer of valueIII. Contingent Functions 6. Basis of credit

7. Liquidity 8. Distribution of national income 9. Guarantor of solvencyI. Primary Functions

1. Medium of exchange:

During the barter system, commodities were exchanged for commodities. In modern times, goods and services are bought and sold with money. Thus, money serves as a medium of exchange.

2. A measure of value:

Money is used to measure the value of goods and services. When the value of goods and services is expressed in the form of money it is called price. When we say that the price of orange is ₹ 50 per kg., we are expressing the value of orange in terms of money. Thus money becomes a unit of account.

II. Secondary Functions

3. A store of value:

Wealth can be stored in the form of money. Thus money serves as an asset or a store of value. Currency held by the people or demand deposits in banks are examples of stores of value.

4. A standard of deferred payments:

Deferred payment is payment after a lapse of time. In other words, deferred payments are future payments. Money is the unit of account in contracts that involve future payments.

5. A transfer of value:

Sale and purchase of goods, property, etc., result in the transfer of value from one person to another. Similarly money facilitates transfer of value from one place to another. Thus, money helps in transferring values.

III. Contingent Functions

6. Basis of credit:

Modern economy and business are based on credit. Money is.the basis of credit.

7. Liquidity:

Liquidity means ready purchasing power, All assets are not liquid, that is, they are not acceptable in all forms of exchange. Money is the most liquid of all assets.

8. Distribution of national income:

Contribution of various factors to national income is expressed in money. Factor rewards are expressed in money. Thus, money facilitates distribution of national income.

9. Guarantor of solvency:

Solvency refers to the ability of a person to pay his debt. If a person fails to honour his obligations, he becomes insolvent. Money guarantees solvency.

Classification of Money The value of money can be classified into three forms. They are 1) full bodied money 2) representative full bodied money 3) credit money. Such a classification is based on the intrinsic value and face value of money. The intrinsic value of money is nothing but the value of the money in terms of the component from which it is being made. The face value of a currency is what it fetches in the market.

1. Full bodied money When the face value of money equals its intrinsic value, money is termed as full bodied money. For example, a gold coin becomes full bodied money when the value of a coin is same as its metal value.

2. Representative Full bodied money The money which has no intrinsic value is called representative full bodied money. Currency notes are examples of representative full bodied money. Currency notes have only face value and no intrinsic value.

3. Credit money The face value of money is greater than the commodity value of the material from which the money is made is called the credit money. The credit money can be classified as follows

a. Token money All coins used in India are token money. Token money has greater face value compared to their intrinsic value. b. Representative token money Representative token money is the representation of money and it is made of paper. c. Promissory notes of central banks It is the paper currency issued by the central bank. All currencies issued by central bank in India are included in this category. d. Bank deposits The demand deposits can be transformed into money by issuing Cheque. (Eg. saving bank account, current account deposits etc.).Demand for Money

Why do People Hold Money with Them? The desire of a person to hold money in hand is called demand for money. Demand for money comes from the fact that money is an asset and acceptable to all. This asset can be easily converted into goods or services. Compared to all other assets, money is the most liquid asset. Wealth in any other form does not have this quality. Money has acceptability all over the world. Money is used for all types of transactions. So people hold money. But when money is kept with us, it has an opportunity cost. The interest forgone on the amount kept as cash is the opportunity cost. So, when money is kept with them, people consider the advantages of liquidity, and the disadvantages of interest forgone.

Demand for money is called liquidity preference. So people’s desire to keep money with them is called liquidity preference or demand for money.

According to J.M. Keynes, “The demand for money is the sum of the money required for transaction motive, precautionary motive and speculative motive”.

(1) Transaction motive

(2) Precautionary motive

(3) Speculative motive

Transaction motive People have to hold money to fulfil their needs. They hold money in this way with the aim of meeting their daily transactions. Keeping money with them to meet their daily expénses is called transaction motive or transaction demand. That is, people keeping cash in their hands to buy goods and services daily is known as transaction demand for money.

How much money should we keep for daily expenditure? This depends on the value or volume of transactions. As the volume of transactions increases transaction demand for money also increases. However, transaction demand for money of an economy is a fraction of the total- volume of the transactions in the economy over a Period of time. It can be written in the form of an equation.

Since \( {v\,={\frac{1}{k}} } \) is the inverse of velocity,

$$ \mathbf{M^{d}_{T}\,=\,kT} $$ $$ \mathbf{∴\, \frac{1}{k}M^{d}_{T}\,=\,T} $$ $$ \mathbf{vM^{d}_{T}\,=\,T\, \Bigl({\mathbf{since\,v\,={\frac{1}{k}}}}\Bigr) } $$ $$ \mathbf{∴\, M^{d}_{T}\,=\,\frac{T}{v}} $$ where, T and v are flow variables.

\( M^{d}_{T} \) is a stock variable.

\( vM^{d}_{T} \) is the total value of transactions of money.

Moreover, this equation states that transaction demand for money is positively related to the value of transactions and negatively related to velocity.

It is important to study the relation between GDP and total transaction demand for money in a year, In an economy, the volume of total transactions during a year is more than nominal GDP, since it includes transactions of all intermediate goods and services. Even then, there is a positive relationship between value of transactions and nominal GDP. An increase in the GDP of an economy means increase in total value of transactions. If so, as GDP increases, transaction demand for money also increases. Therefore, transaction demand for money equation can be written as

$$ \mathbf{M^{d}_{T}\,=\,kPY} $$ where, P = General price level and

Y = Real GDP.

This equation shows that transaction demand for money is positively related to real income and price level.

Suppose in an economy, during a year transactions worth ₹ 2,000 were done with ₹ 500. Here the transaction demand for money is \( M^{d}_{T} \) = ₹500. The value of transactions is T = ₹ 2,000. Since k is the ratio between transaction demand for money and value of

transaction, \( {{k\,={\frac{M^d_T}{T}}}} \) \( {{\,={\frac{500}{2000}}}} \) \( {{\,={\frac{1}{4}}}} \).

Since, velocity of money v is the inverse of k, \( {v\,={\frac{1}{k}} } \)\( {\,={\frac{1}{{\frac{1}{4}}}} } \) = 4. If the velocity is 4, it means that with ₹ 500 four transactions were done. If we know velocity and transaction demand, we can calculate the value of transaction. That is, T= \( vM^{d}_{T} \) = 4 × 500 = ₹ 2,000. This indicates that there are ₹ 2,000 worth transactions of goods and services done in a year.

Precautionary motive People hold money for meeting unexpected contingencies of life. This demand for money is a precaution against uncertainties of life. This is known as precautionary motive.

Speculative Motive People hold their wealth in the form of assets like land, bullion, bonds, securities, etc., expecting a rise in the price of these assets in future. They hold a portion of their income to purchase assets when their prices are low and sell them when their prices rise in order to gain profit. This is called speculation. Speculative demand for money is the desire of the people or institutions to hold money in their hands for speculative purpose.

All forms of assets other than money – land, bullion, goods, shares, securities, etc., are clubbed together into a single category called “Bonds”. Bonds are the promissory notes of a future stream of monetary returns over a period of time. These papers are issued by the government or firms to borrow money from the public and they are tradeable in the market.

Present Value of Bond Present value of a bond refers to the amount to be deposited in savings bank account to earn the same income as from the bond at the existing rate of interest. Attractiveness of a bond depends on its offer price and the present value.

Present value of a bond is calculated as follows:

where,

where,

X = annual income from bond at the coupon rate

y = face value of the bond

r = market rate of interest and

n = maturity period of the bond

Suppose a firm issues a bond at a face value of ₹ 100 with 10% coupon rate of interest for a period of two years. Assume that the rate of interest applicable to savings bank account is 5%. For taking investment decision people compare income from the bond with the interest from the savings bank account. The question here is how much money kept in savings bank account will generate = ₹ 10 at the end of first year?

This is calculated as follows:

Let X be this amount

Then X \( {\Bigl(1+{{\frac{5}{100}}}\Bigr)} \) = ₹ 10

or

Then X \( \frac{10}{\Bigl(1+{{\frac{5}{100}}}\Bigr)} \) = ₹ 9.52

₹ 9.52 is the present value of ₹ 10 discounted at the market rate of interest. i.e., 5%.

Let Y be the amount which if kept in savings bank account will generate ₹ 110 at the end of the second year. Then present value of the returns from the bond will be

PV= X+Y= \( \frac{10}{\Bigl(1+{{\frac{5}{100}}}\Bigr)} \) + \( \frac{10+100}{\Bigl(1+{{\frac{5}{100}}}\Bigr)^2} \)

= \( \frac{10}{1.05} \) + \( \frac{110}{(1.05)^2} \)

= \( \frac{10}{1.05} \) + \( \frac{110}{(1.1025)} \)

= 9.52 + 99.77 = ₹ 109.29

This means that if you deposit ₹ 109.29 in your savings bank account, it will generate the same return as from the bond. In other words ₹ 109.29 is the present value of the bond. But face value of the bond is only ₹ 100. So bond is more attractive than savings bank account and people will go for buying the bond. Increased demand for bond will raise the price of bond. Bond price will increase until it is equal to its present value. If price rises above the present value, bond becomes less attractive compared to the savings bank account. People start selling the bond and bond price comes down until it reaches the present value. Therefore under competitive market condition the price of the bond will be equal to its present value in equilibrium.

A company issues bond with a face value of ₹ 100 at 10% coupon rate of interest for three years. Market rate of interest is 6%. Find present value of the bond.

\( {\,PV\,={{\frac{X}{\Bigl(1+{{\frac{r}{100}}}\Bigr)}}} + {{\frac{X}{\Bigl(1+{{\frac{r}{100}}}\Bigr)^2}}}+…+{{\frac{X+y}{\Bigl(1+{{\frac{r}{100}}}\Bigr)^n}}} } \)

Here

x = \( 100 \,×\frac{10}{100} \) = ₹ 10

y = 100

r = 6%

n = 3

So \( {\,PV\,={{\frac{10}{\Bigl(1+{{\frac{6}{100}}}\Bigr)}}} + {{\frac{10}{\Bigl(1+{{\frac{6}{100}}}\Bigr)^2}}}+{{\frac{10+100}{\Bigl(1+{{\frac{6}{100}}}\Bigr)^3}}} } \)

= 9.4339 + 8.8999 + 92.3593

= ₹ 110.69

Inverse relation between speculative demand for money and rate of interest Different people have different expectations regarding future movement in the market rate of interest. When the interest rate is very high everyone expects it to fall in the future, and the price of bonds to go up. Hence people convert their money into bonds to get capital gain from bonds. Thus, speculative demand for money is low at high interest rate. When interest rate comes down, people expect interest rate to rise and price of bonds to fall in the future, Thus they convert their bonds into money to avoid capital loss. This will give rise to a high speculative demand for money. Hence speculative demand for money is inversely related to the rate of interest. At a higher rate of interest, speculative demand for money is low and at a lower rate of interest speculative demand for money is high. So speculative demand for money can be written as

$$ {\mathbf{M^d_s \,=\,{\frac{r_{max}-r}{r – r_{min}}}}} $$

where \( M^d_s \) is the speculative demand for money. r is the market rate of interest. rmax is maximum or upper limit of r and rmin is the minimum or lower limit of r. rmax and rmin are positive constants. It is evident from the equation that as r decreases from rmax to rmin the value of \( M^d_s \) rises from 0 to ∞.

Liquidity Trap Liquidity trap is a situation in which speculative demand for money is perfectly elastic where the rate of interest reaches the lowest level.

The curve LP is the speculative demand curve for money. It is negatively sloped. When r = rmax speculative demand for money is 0, because everyone converts money into bonds. They think that there will be capital gain through future decrease in interest rates. When r = rmax the economy reaches liquidity trap. Everyone is sure of future rise in interest rate and a fall in bond Price. At the lowest level of interest, the speculative demand for money is infinitely elastic. Because interest decreases and reaches the minimum, everyone expects it to rise in future and hold their money.

The curve LP is the speculative demand curve for money. It is negatively sloped. When r = rmax speculative demand for money is 0, because everyone converts money into bonds. They think that there will be capital gain through future decrease in interest rates. When r = rmax the economy reaches liquidity trap. Everyone is sure of future rise in interest rate and a fall in bond Price. At the lowest level of interest, the speculative demand for money is infinitely elastic. Because interest decreases and reaches the minimum, everyone expects it to rise in future and hold their money.

Aggregate Demand for Money In an economy, the total demand for money (Md) consists of transaction demand \( M^d_T \) and speculative demand \( M^d_s \) . Transaction demand is directly proportional to real GDP and price level. Speculative demand is inversely related to market rate of interest. The aggregate demand for money in an economy can be summarized by the following equation.

$$ \mathbf{ M^d \,=\,{M^d_T + M^d_s}} $$ $$ \mathbf{M^d \,=\,kPY\,+\,{\frac{r_{max}-r}{r – r_{min}}}} $$

Supply of Money Money supply refers to the total amount of money available in the economy. In other words, it is the total volume of money held at a specific point of time by the public, businessmen, and firms for transactions. But the cash balance in government treasuries, central banks and the cash reserve of commercial banks held by the RBI do not come under money supply. On the other hand, the coins and currency notes held by the people, demand deposits in bank and time deposits are part of the supply of money. So the total volume of money in circulation and which can be spent by the people at a specific point of time in an economy is money supply. Money supply indicates the total purchasing power in the economy.

Legal Definitions

Narrow and Broad Money The Reserve. Bank of India publishes four different measures of money supply under the heads, M1, M2, M3, and M4, from April 1st 1977. They are defined as given below:

Legal Tender is legal medium of payment recognised by a legal system to meet financial obligations. Coins and banknotes are legal tender, but cheques and such non cash payments are not usually legal tender.

Money Creation by the Banking System Here we shall discuss the determinants of money supply.

Different actions of the Central Bank and the commercial banks influence money supply. cdr, rdr, CRR, SLR and Bank rate are the important factors that influence money supply.

(1) Currency Deposit Ratio (cdr) cdr is the ratio of money held by the public in currency to the deposits they hold in banks,

$$ \mathbf{cdr\,=\,\frac{CU}{DD}} $$ If a person gets one rupee, he deposits \( {\frac{1}{1+cdr}} \) in the bank and keeps \( {\frac{cdr}{1+cdr}} \)in cash. cdr is the reflection of the liquidity preference of the people. Since expenditure is high, people convert their demand deposit into money during festival seasons and hence cdr increases.

Suppose in an economy, the money held in hand by the people is ₹ 200 crore and demand deposit is ₹ 1,000 crore.

Then,

\( \mathbf{cdr\,=\,\frac{CU}{DD}} \) = \( \mathbf{=\,\frac{200}{1000}} \) = 0.2

The total money supply is M1 = CU + DD = 200 + 1,000 = ₹ 1,200 crore. If we know the cdr and the total supply of money we can find demand deposit and currency with the people. That is, M1 = 1,200, cdr = 0.2 then Demand deposit is

\( {DD\,=\,\frac{1}{1 + cdr}×\,1200 } \)

\( {=\,\frac{1200}{1 + 0.2}} \)

\( {=\,\frac{1200}{1.2}} \)

= ₹ 1000 crore. Currency with the people is

\( {CU\,=\,\frac{cdr}{1 + cdr}×\,1200 } \)

\( {=\,\frac{0.2×1200}{1 + 0.2}} \)

\( {=\,\frac{240}{1.2}} \)

= ₹ 200 crore.

(2) Reserve Deposit Ratio (rdr) Commercial banks accept different types of deposits from the public. A portion of this is kept as reserve. The ratio between the reserve money and the total deposit is rdr. That is, the ratio of cash reserves kept by commercial banks and total deposits in the bank is rdr.

$$ \mathbf{{rdr\,=\,\frac{Reserve}{Total\,Deposit}} {=\,\frac{R}{DD}}} $$

Bank uses a portion of this reserve when the accountholders demand money. The rest of it is used to give loans and make investments.

The reserve money of commercial banks has two parts.

(1) Vault cash: Money kept in their safes for daily transactions.

(2) Reserve with RBI: The portion of money kept by commercial banks with the RBI. Reserve kept by commercial banks as per instructions of the RBI is of two kinds: (a) Cash Reserve Ratio:The fraction of reserve money kept in RBI by commercial banks as a ratio of their demand deposits is called CRR.

(b) Statutory Liquidity Ratio:A given fraction of total demand and time deposits of commercial banks invested in the form of specified liquid assets such as government securities is called SLR.

- The interest paid to the depositor by commercial banks is called borrowing rate.

- The interest charged by commercial banks on loans advanced to individuals and institutions is called the lending rate. Lending rate will always be more than borrowing rate.

- The difference between borrowing rate and lending rate is the bank’s profit and is known as spread.

High Powered Money (H) High powered money is the total liability of the monetary authority. This is the money injected by the monetary authority of a country (RBI) in the economy. It is also called monetary base or money base.

High powered money consists of (1) currency (notes and coins in circulation with the public and vault cash of commercial banks) and (2) deposits held by commercial banks and the Government with RBI. High powered money is currency plus reserves.$$ \mathbf{H \,= \,CU \,+ \,R} $$

Where, H = High powered money CU= Currency R = Reserve moneyMechanism of Money Creation by the Reserve Bank Commercial banks play an important role in the process of money creation, This mechanism of money creation by the monetary authority (RBI) can be explained with help of an example.

Suppose RBI wants to increase money supply by ₹H. For this the RBI buys some assets like Government bonds and gold for ₹H from the market and issues a cheque worth ₹H to the seller of the bond. Assume cdr = 1 and rdr = .2. The seller encashes the cheque ₹H from bank A and deposits ₹ \( \frac{H}{2} \) the same bank and encashes the balance ₹ \( \frac{H}{2} \) Thus the currency held by public goes up by ₹ \( \frac{H}{2} \) and the liability of the bank A goes up by ₹ \( \frac{H}{2} \) because of the rise in deposits.

The assets of the bank increase in the form of the cheque which is the claim on the RBI. Thus the liability of RBI goes up by ₹ H which is the sum total of the claims of bank A and the seller of the bond. So the high powered money increases by ₹ H. This process does not end here. Bank A keeps ₹ \( \frac{.2H}{2} \) as reserve and gives loan ₹ \( \frac{.8H}{2} \) to another borrower. i.e., Bank A gives loan 80% of the total deposits after keeping 20% as reserve. The borrower invests the money in some projects and makes payment connected with the project.

Let us suppose that a worker in the project gets this Payment and keeps ₹ \( \frac{.8H}{4} \) as cash, and deposits ₹ \( \frac{.8H}{4} \) in bank B. Bank B keeps ₹ \( \frac{.16H}{4} \)as reserve, and lends ₹ \( \frac{.64H}{4} \) to a second borrower. Then the second borrower invests this money in any project and pays it as factor payments. A second worker who gets this money keeps ₹ \( \frac{.64H}{8} \) as cash, and deposits the rest ₹ \( \frac{.64H}{8} \) in bank C. This process continues ad infinitum.

After several rounds, this money becomes too small. In the subsequent round it cannot practically contribute anything to the total volume of money supply. The round effect of money supply is called convergent process.

| Table 9.1 | ||||||

|---|---|---|---|---|---|---|

| Rounds | Currency | Deposits | Money Supply [M = CU + DD] |

|||

| Round 1 | \( \mathbf{\frac{H}{2}} \) | \( \mathbf{\frac{H}{2}} \) (Bank A) | \( \mathbf{\frac{H}{2}} \) + \( \mathbf{\frac{H}{2}} \) = H | |||

| Round 2 | \( \mathbf{\frac{.8H}{4}} \) | \( \mathbf{\frac{.8H}{4}} \) (Bank B) | \( \mathbf{\frac{1.6H}{4}} \) = .4H | |||

| Round 3 | \( \mathbf{\frac{.64H}{8}} \) | \( \mathbf{\frac{.64H}{8}} \) (Bank C) | \( \mathbf{\frac{.64H}{4}} \) = .16H | |||

| . . |

. . |

. . |

. . |

|||

| Sum | \( \mathbf{\frac{5H}{3}} \) | |||||

Table 9.1 gives this process which gives an idea of how the money supply in the economy is changing round after round. In order to find out the total increase in money supply, we must add up money supply in each round. i.e.,

M = H + 0.4H + 0.16H + 0.064H + …. ∞

= H[1 + 0.4 + 0.16 + 0.064 + … ∞] = H[1+ 0.4 + (0.4)2 + (0.4)3 + … ∞] The items in brackets are an infinite geometric series. To find the sum of infinite geometric series we can use the equation \( {\frac{a}{1 – r}} \) Where a is the first term r = common factor. Since a = 1, and r = 0.4 \( M\,=\,H\,×\,{\frac{1}{1-0.4}} \) = \( {\frac{5H}{3}} \) The increase in total money supply is \( {\frac{5}{3}} \) times of high powered money. RBI initially injected H money in the economy. Now the supply of money exceeds the amount of high powered money initially injected by the RBI.Money Multiplier The ratio of stock of money to the stock of high powered money in the economy is called money multiplier. It measures the number of times money supply increases due to an initial increase in high powered money. For example, suppose when RBI injected ₹ 100, money supply increased to ₹ 400. So money supply increased 4 times of ₹ 100. So the money multiplier is 4.

We can calculate money multiplier by dividing total money supply by high powered money. $$ \mathbf{Money\,multiplier\,={\frac{M}{H}}} $$ Value of money multiplier depends on cdr and rdr. We can also calculate money multiplier by using the following equation:

$$ \mathbf{Money\,multiplier\,={\frac{M}{H}}= {\frac{1+cdr}{cdr+rdr}}} >1 $$In an economy cdr = 1, rdr = .2, Then money multiplier, M/H = (1 + 1) / (1 + .2) = 2 / 1.2 = 1.66. This means that if RBI injects ₹ 1 in the economy it will go up by ₹ 1.66.

Central Bank Every country has a central bank. The Central Bank is the apex institution of a country’s monetary system. India’s Central bank is the Reserve Bank of India. RBI came into existence in 1935. Important functions of the Central bank are briefly described below:

(1) Issue of Currency The Central bank is the monetary authority. It has monopoly power of printing and issuing currency-notes. RBI in India prints all denominations of currency notes except one rupee notes. One rupee notes and coins are issued by the Finance Ministry, Government of India.

(2) Bankers’ Bank The Central bank functions as the bank of banks. It controls commercial banks and other financial institutions. In times of need, the Central bank provides assistance to commercial banks. That’s why the Central bank is called banker’s bank.

(3) Banker to the Government The Central bank is the banker to the government. It performs all the banking business of the government. The Central bank accepts money and makes payments on behalf of the government as its agent. It also advises the government on monetary matters.

(4) Controller of Money Supply Another important function of the Central bank is to act as the controller of money supply. The Central bank controls the total size of money supply and credit. It maintains economic stability by changing bank rate, cash reserve ratio, etc.

(5) Custodian of Foreign Exchange The Central bank is the custodian of the foreign exchange reserves of the nation. Gold reserves of the nation are also kept by the Central bank.

(6) Lender of Last Resort When commercial banks face financial crisis, RBI plays a crucial role. Commercial banks approach the – RBI for assistance as a last resort. When RBI extends helping hand to commercial banks in times of financial difficulties, RBI may be called lender of the last resort.

(7) National Clearing House The Central bank acts as a clearing house for transfer and settlement of mutual claims of commercial banks. Bank to bank clearing and settlement through the central bank is easy since the Central bank holds cash reserves of commercial banks.

(8) Publication of Report Another important function of the Central bank is publication of reports on banking, currency, finance and macroeconomy. In India the RBI publishes reports on important economic and financial indicators.

Monetary Policy and Instruments of Monetary Policy The Central bank formulates the monetary policy of the country. Main objectives of the monetary policy are price stability, reduction of unemployment and economic growth. Measures taken by the monetary authority to control supply of money constitute monetary policy. Monetary policy aims at controlling money supply thereby regulating the availability and cost of credit.

Following are the instruments of monetary policy:(1) Repo Rate Repo rate is the rate at which the central bank lends money to the commercial banks. Repo rate is the effective instrument of monetary policy used by the central bank to achieve price stability and economic growth. During times of inflation, the central: bank will raise the repo rate thereby raising the cost of funds. This will reduce aggregate demand and control inflation. During deflation/ recession, the central bank will reduce the repo rate. Lower rates will stimulate growth in the economy.

(2) Reverse Repo Rate Reverse repo rate is the interest rate received by the commercial banks for parking money with the central bank. In other words, Reverse repo rate is the rate at which the central bank borrows from commercial banks. Normally, reverse repo rate goes up and down along with the repo rate.

Marginal Standing Facility (MSF)

Marginal Standing Facility (MSF) is a new instrument of monetary policy introduced by the RBI in 2011. MSF is a facility for banks to borrow from the RBI in an emergency, when inter-bank liquidity dries up completely. Under MSF banks borrow from the RBI by pledging government securities at a rate higher than the repo rate.

Presently (Jan 2022) the-repo rate is 4.00 %, the reverse repo rate is 3.35 % and MSF rate is 4.25 %.

(3) Reserve Ratios Another instrument to control money supply is Reserve ratio. Bringing about suitable changes in CRR and SLR, money supply can be controlled. During inflation, by increasing CRR and SLR, credit availability is reduced and thereby money supply is reduced. During deflation, on the other hand, CRR and SLR are reduced and banks’ lending capacity increases.

(4) Open Market Operations Open market operations refer to the purchase and sale of Government securities by the RBI. During inflation, the RBI sells securities. The securities are mainly bought by commercial banks. When commercial banks buy securities the money in their hands reach the RBI. Then the capacity of the commercial banks to lend money is reduced. The excess money with the public reaches the RBI. During deflation, the RBI buys back the securities. Then money comes back to commercial banks. This increases availability of money in the economy.

Regulations of money supply by the RBI can be summarised as follows:

| Table 9.2 | ||

|---|---|---|

| Instruments | Inflation | Deflation |

| Bank Rate | Increases | Decreases |

| CRR | Increases | Decreases |

| SLR | Increases | Decreases |

| Open Market Operation | Sells Securities | Buys Securities |

Sterilization Sterilization is the intervention by the monetary authority of a country in the money market to keep money supply stable against exogenous or sometimes external shocks such as an increase in foreign exchange inflow.

Due to better growth prospects in India, investors from abroad increase their investments in Indian securities (shares of Indian companies and bonds issued by government), Foreigners will buy these securities with foreign currency. Theperson who sells these securities to foreign investors will exchange his foreign currency into Indian rupee through a commercial bank. This will increase the total supply of money in the economy. The bank in turn, will submit this foreign currency to RBI and its deposit in RBI will be credited with equivalent sum of money. To compensate for the increase in money supply, the RBI sells securities in the open market. The value of securities sold will be exactly equal to the increase in money supply caused by the foreign investment. Through this selling of securities the RBI absorbs the excess money supply in the financial system. Thus, the total money supply and the stock of high powered money remain the same. Thus, RBI intervenes in the money market to keep the money supply stable against exogenous or external shocks. This process is known as sterilization.

Functions of Commercial Banks Commercial banks are very important institutions in modern economy. These financial institutions perform several functions like accepting deposits, giving credit, and other functions that provide facilities for business and trade. The functions of commercial banks can be described as given below:

I. Primary Functions

(1) Accepting Deposits The traditional and important function of commercial banks is accepting deposits. Commercial banks usually accept three types deposits from the public:

(a) Savings Deposit (b) Current Deposit and (c) Fixed Deposit.

(2) Giving Credit Commercial banks give loans to those who need them on security. Credit is given as cash credit, call loan, overdraft, etc. Loans given as cash on the security of material assets is cash credit. Loans which are to be repaid on call, are called call loans. Overdraft is another facility given to the customers. It allows the account holders to draw from the bank amount higher than the cash balance in their accounts.

(3) Discounting Bills of Exchange A customer with a bill of exchange can, in times of need, approach a commercial bank for money. The bank will give money after discounting the bill of exchange.

(4) Credit Creation Commercial banks can create credit. A person approaches a bank for a loan. The bank sanctions the loan on proper security. But the loan amount is not given directly to the borrower. Instead, it is deposited in the name of the same borrower. Thus, every loan creates a deposit.

(5) Investment After giving loans the banks will still have money left with them. This excess money is invested. Banks are bound by law to invest a part of their deposits in Government approved securities. So investing is an important function of commercial banks. Banks usually invest their funds in Government securities and other approved securities.

II. Secondary Functions The secondary functions can be classified under two heads:

(a) Agency Functions Bank works as an agent of the customers and charges commission.

(i) Transfer of Funds: Banks transfer money from one place to another through Drafts, Mail Transfer, Electronic Transfer, etc. (ii) Collection of money: On behalf of the customers, banks collect money through cheque, draft, etc. (iii) On behalf of the customers, banks collect dividends on shares, and interest on debentures and bonds. (iv) On behalf of the customers at pay bill amount, surance premium, ete. In addition to this banks also take up purchase. and sale of shares and financial securities. (v) Executes wills of customers.(b) Miscellaneous Functions 1. Purchase and sale of foreign currency

2. Issue of Travellers’ cheque, gift cheque, etc. 3. Offer safe deposit facilities to keep precious things 4. Issue of letters of credit 5. Issue of ATM card, Credit card and Debit card 6. Underwriting of financial securities like shares during public issue (underwriting is taking up purchase of a part of unsold securities in public issue) 7. Tele banking 8. Internet bankingIII. Development Functions 1. Loans to the weaker sections at low rates of interest

2. Loans to the unemployed to find employment 3. Loans for priority sector From the above mentioned functions of commercial banks it is very clear that they play a vital role in modern economies. ![]()

0 Comments