Plus Two Economics Chapter 1

Chapter 1

Introduction:

The word ‘Economics’ has been derived from the Greek word Oikonomia which means ‘household management’. In early days Economics was known as Political Economy. Alfred Marshall for the first time used the term Economics instead of Political economy’. It was with the publication of Adam Smith’s (Father of Economics) famous book “An Enquiry into the Nature and Causes of Wealth of Nations” (1776) that economics became an independent discipline.

Definitions:

Wealth Definition

Adam Smith (1723 -90) defined economics as follows : ‘Economics is the science of wealth’. He is the author of the famous book “An Enquiry into the Nature and Causes of Wealth of Nations” also known as ‘Wealth of Nations’ was published in the year 1776. He is known as the Father of Political Economy because he was the first person who put all the economic ideas in a systematic way. It is only after Adam Smith, we study economics as a systematic science.

“Economics is the study of nature-of wealth, its generation and spending”

– Adam Smith

Welfare Definition

This definition expands the field of economic science to a larger study of humanity. Specifically, Marshall’s view is that economics studies all the actions that people take in order to achieve economic welfare. In the words of Marshall, “man earns money to get material welfare.” Others since Marshall have described his remark as the “welfare definition” of economics. This definition enlarged the scope of economic science by emphasizing the study of wealth and humanity together, rather than wealth alone. His famous publication “Principles of Economics” was published in the year 1890.

“Economics is a study of mankind in the ordinary business of life; It examines that part of individual and social action which is most closely connected with the attainment and with the use of the material requi- sites of well-being. Thus, it is on the one side, a study of wealth; on the other and more important side, a part of the study of man.”

— Alfred Marshail

Scarcity Definition

In his publication, “Essay on the Nature and Significance of Economics”in 1932, British economist Lionel Robbins defined the discipline in terms of scarcity:

“Economics is a social science which deals with human behaviour as a relationship between ends and scarce means which have alternative uses.”

– Lionel Robbins

Growth Definition

Paul A Samuelson, while recognizing scarcity factor and resource management, gave importance to economic growth. He is the author of the book “Economics” published in 1964.

“Economics is the study of how men and society choose, with or without the use of money, to employ scarce productive resources which could have alternative uses, to produce various commodities over time and distribute them for consumption now and in the future among various people and groups of society.”

— Paul A. Samuelson

The growth definition is widely regarded as the modern definition of economics.

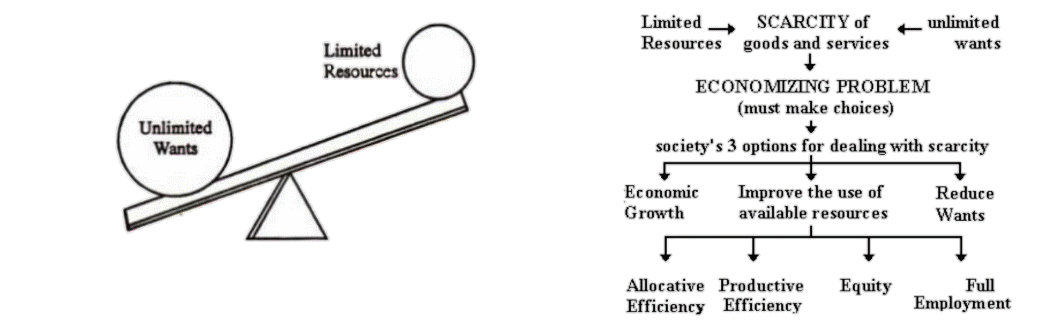

Human wants are unlimited and the resources are limited. Therefore Economics is the study of choice and prioritisation of our wants in the presence of scarce resources.

Human wants are unlimited and the resources are limited. Therefore Economics is the study of choice and prioritisation of our wants in the presence of scarce resources.

So, Economics is a branch of knowledge which is concerned with the production, consumption, and distribution of wealth. Fundamental problems of an Economy is related to the above economic activities.

So, Economics is a branch of knowledge which is concerned with the production, consumption, and distribution of wealth. Fundamental problems of an Economy is related to the above economic activities.

Simple Economy

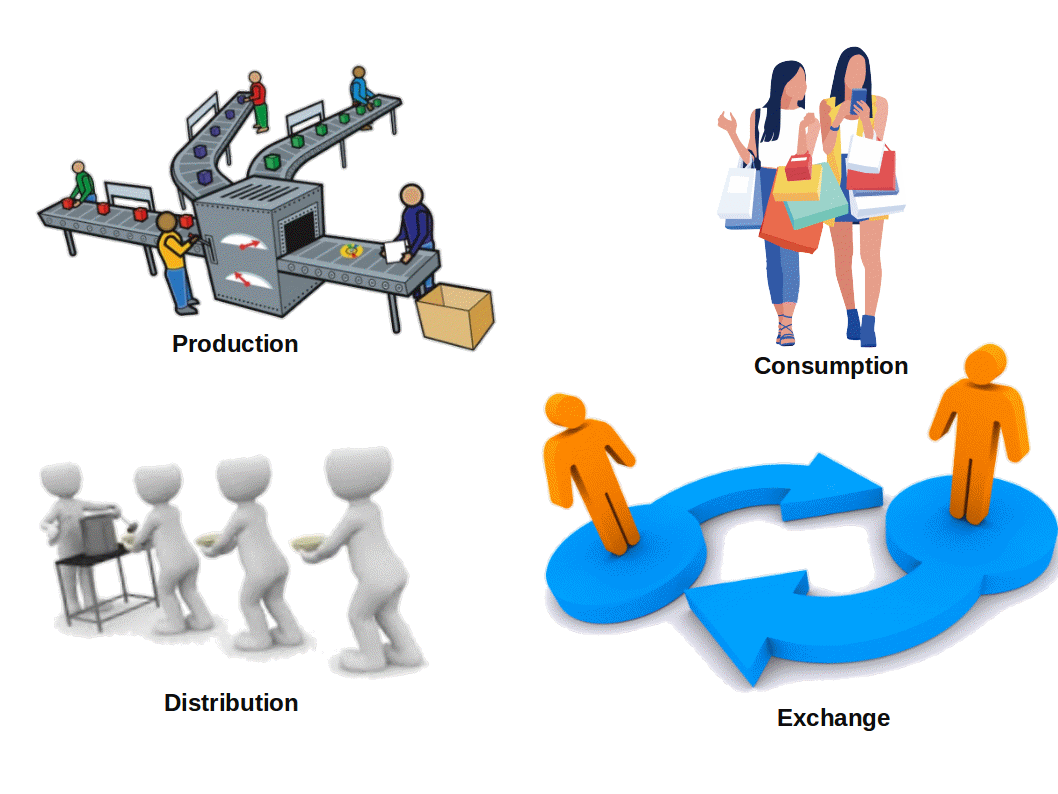

An economy can be perceived as an area of production, distribution, trade and consumption of goods and services by different economic agents in a given geographical location. Economic agents can be individuals, business organisations or governments. They are engaged in various economic activities.

Economics deals with the day-to-day economic activities such as production, consumption, capital formation, exchange and distribution of goods and services. Therefore, we can define economics as a social science which studies the economy and economic activities.

Economic System

Economy in the large set of interrelated production and consumption activities that aid in determining how scarce resources are allotted. This is also known as Economic System.

Central Problems of an Economy

Production, consumption, exchange and distribution of goods and services are the basic economic activities. Every society faces the problem of scarcity of resources and that leads to the problem of choice. Therefore, choice is the central problem of any economy, There are four main reasons for economic problems in an economy, They are:

- Human wants are unlimited

- Resources are limited

- Resources have alternative uses

- Resources have different priorities

1. What to produce and in what quantities?

Every society wants thousands of goods and services. Since resources are scarce, all these goods and services cannot be produced. Therefore, it has to decide what type of goods should be produced, whether to produce more food or goods for national security or to have more of luxury goods. It has to prioritise and decide what to produce and how much to produce. For example, if it is decided to produce rice, then how many tons of rice are to be produced in an economy.

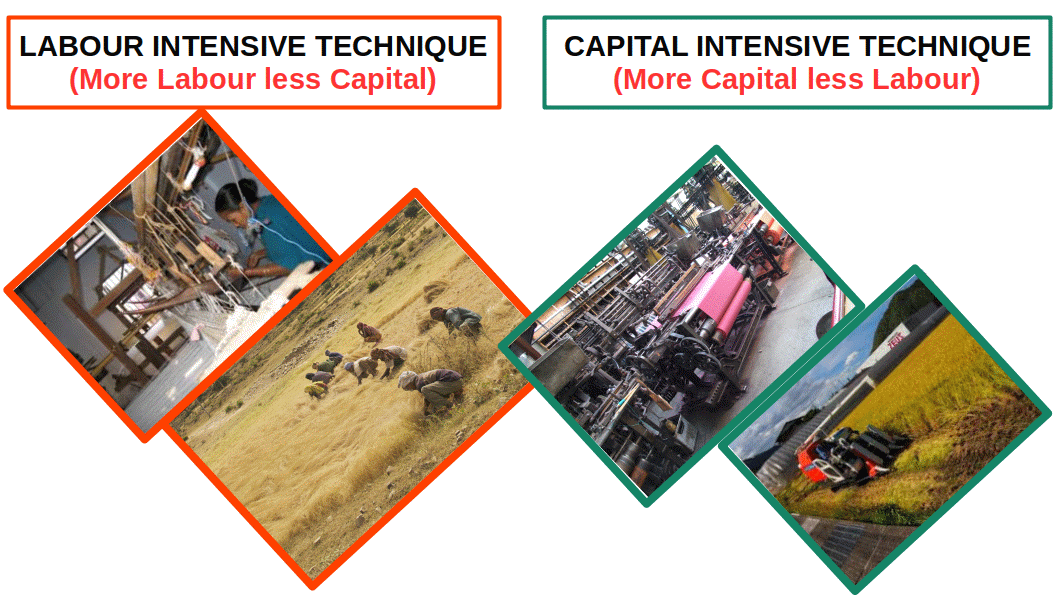

2. How to produce?

After the decision of what and how much to produce, the next step is how to produce the chosen goods. The question “How to produce” implies which methods or techniques of production are to be used, i.e., whether to choose labour-intensive techniques or capital intensive techniques of production. The choice of technique of production depends on the availability and price of labour and capital in the economy. It is beneficial to choose less expensive techniques of production.

Labour Intensive Technique of Production is the technique which uses more labour and less capital.

Labour Intensive Technique of Production is the technique which uses more labour and less capital.

Capital Intensive Technique of Production is the technique which uses more capital and less labour.

| Table 1.1 Merits and Demerits of Labour Intensive Production Technique. | ||

| Merits | Demerits | |

|---|---|---|

| Labour intensive technique provides more employment Opportunities. | Labour intensive technique is less productive. | |

| Labour intensive technique needs less capital. | Labour intensive technique prevents development. | |

| Labour intensive technique requires less skill only. | Labour intensive technique makes the economy less productive. | |

3. For whom to produce?

For whom to produce means the functional distribution of output. It implies the distribution of output (income) amongst the owners of the factors of production, i.c., the distribution of rent, wages, interest and profit amongst the owners of land, labour, capital and organisation respectively. This is called functional distribution of output.

Every economy should find the answers to the three above stated questions. In other words, the allocation of scarce resources, full utilisation of resources, growth of resources and efficiency in production and distribution are the basic economic problems of any economy.

| Table 1.2 Rewards of Factors of Production | ||

| Land | Rent | |

|---|---|---|

| Labour | Wage | |

| Capital | Interest | |

| Organisation | Profit | |

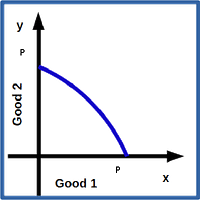

Production Possibility Curve (PPC) or Production Possibility Frontier (PPF)

PPC is also known as production transformation curve. It is a statistical device used to represent the central economic problems such as allocation, full utilisation and growth of resources and efficiency in production and distribution. It is defined as the locus of points of combinations of two goods which an economy can produce with the available resources and the given level of technology.

In the above diagram OX axis and OY axis represent quantities of corn and cotton. Curve AE is the PPC. A, B, C, D and E are the various combinations of good 1 and good 2.

Production Possibility Set

Production possibility set is a set of all combinations of two goods say Good 1 and Good 2.

Suppose, in an economy only two goods are produced, viz, cotton and corn. Some production possibilities of cotton and corn are given in the following Table 1.2.

| Table 1.3 Production Possibility Table | ||

| Production Possibilities | Cotton | Corn |

|---|---|---|

| A | 10 | 0 |

| B | 9 | 1 |

| C | 7 | 2 |

| D | 4 | 3 |

| E | 0 | 4 |

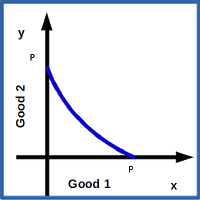

When all such production possibility combinations are plotted on a graph and joined together we get a Production Possibility Curve (PPC).

In the graph, corn is shown along x-axis and cotton along y-axis. AE is called PPC. A,B,C,D and E are the various production possibilities.

Features of PPC

- It is a downward sloping curve from left to right.

- It is concave to the origin.

Graphical Presentation of Central Economic Problems

We can explain the basic problems of an economy with the help of a PPC.

In the above given diagram PP is Production Possibility Curve. Any point on the PPC, such as P, Q, R, S, shows full and efficient utilisation of resources. Any point like U inside the PPC shows under or partial utilisation of resources or inefficiency. The curve P’P’ shows growth of the economy and an increase in productivity. The rightward shift of the PPC indicates increase in resources and consequent growth of the economy.

Opportunity Cost

In economics, Opportunity Cost is very important. Opportunity cost of a product or service can be defined as the next best alternative product or service that has been sacrificed or forgone. The opportunity cost of a decision is the next best alternative we give up to get what we want. Table 1.2 reveals that the opportunity cost of 10 units of otton is 4 units of corn or the opportunity cost of 4 units of corn is 10 units of cotton sacrificed and forgone.

Marginal Opportunity Cost – MOC

Marginal opportunity cost means the additional cost in terms of a number of units of good sacrificed to produce an extra unit of other good.

Algebraically, \( \mathbf {MOC_x ={{{\frac{ΔY}{ΔX}} }}} \)

where,

ΔY = Change in the quantity of good Y

ΔX = Change in the quantity of good X

| Table 1.4 Marginal Opportunity Cost | ||||

| Production Possibilities | Cotton | Corn | MOC of Wheat | Method of Calculation MOC of Wheat |

|---|---|---|---|---|

| A | 10 | 0 | – | — |

| B | 9 | 1 | 1 | 10-9 ÷ 1-0 = \( \mathbf {{{{\frac{1}{1}} }}} \) = 1 |

| C | 7 | 2 | 2 | 9-7 ÷ 2-1 = \( \mathbf {{{{\frac{2}{1}} }}} \) = 2 |

| D | 4 | 3 | 3 | 7-4 ÷ 3-2 = \( \mathbf {{{{\frac{3}{1}} }}} \) = 3 |

| E | 0 | 4 | 4 | 4-0 ÷ 4-3 = \( \mathbf {{{{\frac{4}{1}} }}} \) = 4 |

Relation between Marginal Opportunity Cost (MOC) and Production Possibility Curve (PPC)

There is an important relationship between MOC and PPC. MOC may increase, decrease or remain the same. When MOC increases PPC becomes Concave to the origin, and a decrease in MOC turns the PPC into Convex, When MOC remains constant, PPC becomes Linear.

| Table 1.5 Relation between MOC and PPC | ||

| MOC | PPC | Shape |

|---|---|---|

| Increasing |  |

Concave to origin |

| Decreasing |  |

Convex to origin |

| Costant |  |

Linear |

Organisation of Economic Activities

Every economy tries to solve central problems of the economy in different ways. Now we can see how solutions to central economic problems are found in different economic systems.

Centrally Planned Economy (Socialist Economy)

It is an economic system where all means of production are under the ownership and control of the government.

In centrally planned economies or socialist economies, the planning authority or the Government decides important issues like what to “produce, how to produce and for whom to produce. In these economies most of the resources are in the public sector. Through control of resources, the Government or the planning authority decides what to produce and what not to produce. The Government also does the distribution of goods and services. Through such a policy the Government ensures the welfare of the common people.

Features of Centrally Planned Economy (Socialist Economy)

- Public Ownership

- Central Planning

- Definite Objectives

- Freedom of Consumption

- Equality of Income Distribution

- Welfare motive

Market Economy (Capitalist Economy)

It is an economic system in which all means of Production are under the ownership and control of private individuals.

In Market Economy or Capitalist Economy, the market mechanism or price mechanism decides what to produce, how to produce and for whom to produce. The producers as well as the consumers decide, through the forces of demand and supply, what to produce, how to produce and for whom to produce. In fact, the market takes decisions on utilisation of resources, distribution of goods and services and their efficiency.

Features of Market Economy (Capitalist Economy)

- Private property

- Freedom of enterprise

- Profit motive

- Price mechanism

- Consumer sovereignty

- Free trade

Mixed economy

It is an economic system where all means of production are under the ownership and control of both government and private individuals. It is a mixture of salient features of socialism and capitalism.

Most of the economies in the world are mixed economies. Under mixed economy, public and private sector work together. In a mixed economy all the central problems of what to produce, how to produce and for whom to produce are solved by both planning authority and price mechanism. The private sector works with a profit motive, whereas the public sector aims at social welfare.

| Table 1.6 Comparative study of socialist, capitalist and mixed economy | ||

| Socialist Economy | Capitalist Economy | Mixed Economy |

|---|---|---|

| All means of production are under the ownership and control of government | All means of production are under the ownership and control of private individuals | All means of production are under the ownership and control. of both private individuals and government |

| Economic equality, equal opportunity | Individual freedom, freedom of enterprise | Co-existence of public and private sector |

| Economic planning | Price mechanism | Economic planning and price mechanism |

| Welfare motive or social welfare | Profit motive and consumers sovereignty | Social welfare and profit motive |

Positive and Normative Economics

Economic analysis is of two types. They are positive economics and normative economics. A positive economics deals with ‘what is’. e.g.,Unemployment level is high in India. A normative economics deals with ‘what ought to be’. e.g., Population growth in India affects economic growth. In positive analysis, the consequences of an action are explained without going into its merits and demerits. In normative analysis, the desirability or other- wise of an action is analysed. Thus, in positive economic analysis the consequences of an economic policy or decision are studied. Results are analysed without passing moral judgements. In normative economic analysis, the results of an action are analysed by examining whether they are desirable or not. For a proper understanding of economic issues, we need both positive and normative economic analysis.

| Table 1.7 Positive and Normative Economics | ||

| Positive Economics | Normative Economics | |

| What is …? | What ought to be …? | |

|---|---|---|

| No evaluation of merits and demerits | Openly discusses the merits and demerits | |

Microeconomics and Macroeconomics

Economic theory is classified into Microeconomic theory and Macro-economic theory.

The word micro is derived from the Greek word Mikros which means small. Microeconomics is the study of parts of the economy or individual units of the economy. Micro- economics studies the behaviour of a consumer or a producer or the individual prices of a product. It studies the theories of demand, production, cost, the theory of factor pricing, the theory of welfare and the price theory, etc.

The word macro comes from the Greek word Makros which means large. Macroeconomics is the study of the economy as a whole. It is also called Aggregate Economics or Income Theory. Aggregate economic units like national income, aggregate demand, aggregate supply, general price level, total employment, etc., come under macroeconomics. Topics like monetary theory, trade cycles, theory of growth and international trade come under macroeconomics.

Microeconomics can be compared to the study of trees while macro-economics can be compared to the study of forest. Methodology of microeconomics is Partial Equilibrium whereas the methodology of macroeconomics is General Equilibrium. Microeconomics gives a ‘worm’s-eye-view’ of the economy while macro-economics gives a ‘bird’s-eye-view’ of the economy.

| Table 1.8 Difference between Micro and Macro Economics | ||

| Basic | Micro Economics | Macro Economics |

|---|---|---|

| Unit of study | Consumers, households, firms, etc. | GDP, price level, etc. |

| Method | Partial equilibrium | General equilibrium |

| Scope | Simple micro unit | Aggregate economy |

| View point | Worm’s eye view | Bird’s eye view |

| Objective | To analyse the behaviour of individual economic units | To analyse the behaviour of the economy and its aggregate |

| Example | Individual demand, Individual income, etc. | Aggregate demand, national income, etc. |

![]()

0 Comments